What Makes It more likely?

How to spot risks?

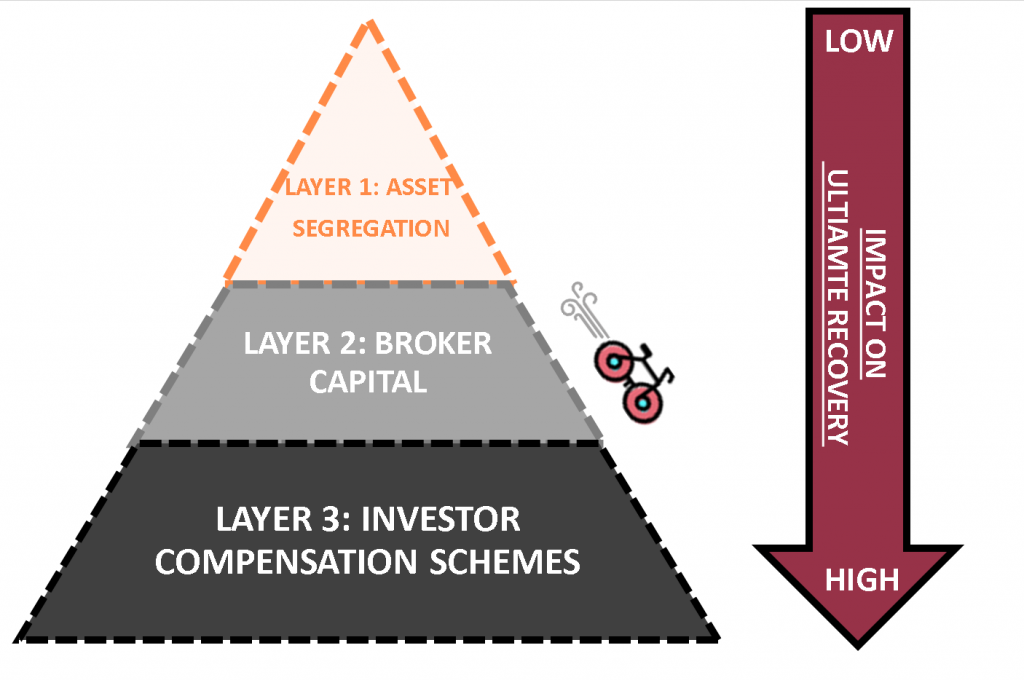

What Is the Potential Damage?

The broker does not hold shares in your name with the custodian.

Although old terms such as ‘deposit’ or ‘safekeeping’ are still used, shares have not been held in paper form for many years.

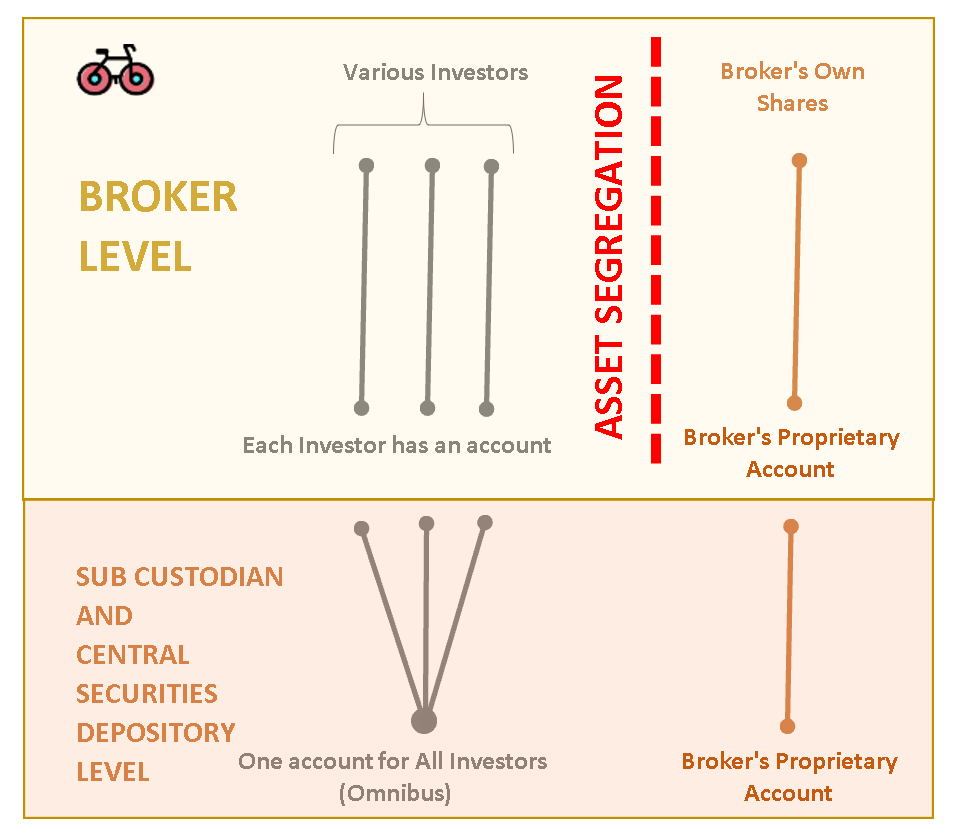

Your shares are commingled with other investors in a Central Securities Depository that tracks the ownership of shares. Because Omnibus accounts are used in most cases, your name won’t be listed on this depository, but rather your broker or another executing broker that executed the order for them as the ‘Nominee’, as illustrated below.

But remember, at the Central Securities Depository level, all of these client assets are held together. So, a chain of rights is in place, in which you, the investor, are the ultimate beneficiary. But, this assumes the broker’s accounting system, at the moment of bankruptcy, has all the relevant information, which is not a guarantee. Bankruptcies happen for a reason, and accounts can be manipulated.

No. In fact, the scheme was mainly designed to protect securities, not cash, that won’t be returned to investors due to fraud. That’s because Investors are supposed to make money work for them by purchasing securities, and not hold cash. But fortunately, the ICS also happens to cover any remaining cash up to the overall limit.

In the best case, if broker systems are good, and there is no fraud, the transfer of shares to another broker will be much smoother. But unfortunately, asset segregation is not a guarantee and is unlikely to provide protection when you need it most.

Asset segregation is designed to keep client assets separate to avoid the commingling of customer assets with the working capital of the brokerage firm. The process involves having separate legal entities, e.g. an SPV, that is bankruptcy-remote from the Broker and can’t be accessed by broker creditors during an insolvency process.

So yes, all brokers will claim asset segregation, because it’s a regulatory requirement. But the broker is managing all accounts until it collapses. This protection only works if the employees of the broker don’t act in a fraudulent manner by mismanaging, including in the accounts, client assets of the separate entity, including transferring/selling or mismanaging your shares.

But, when the Broker is on the edge of collapse, and needs cash or assets to meet its own liabilities, the temptation to ‘borrow’ client assets, may become appealing.

This is usually not the case. Cash is protected up to the combined amount. That’s because it’s likely that the cash is held by the broker in a commingled custodian account along with other investors.

The reason is simple. Investors shouldn’t hold cash in their broker accounts, but rather money market funds or other short-term instruments.

But there is one exception. Certain brokers are affiliated with banks and if they do open an account in your name, then the EU Deposit Guarantee Scheme will protect you up to an additional €100k.

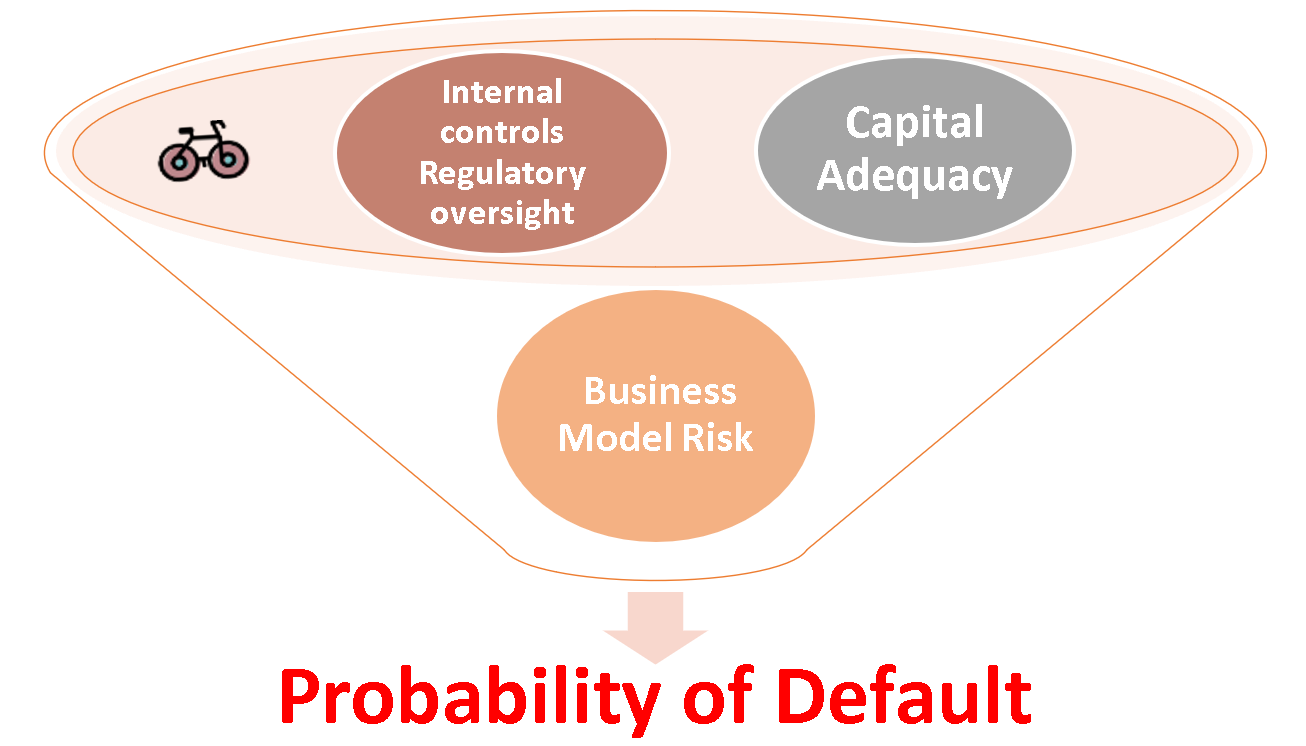

Indeed, most individual investors don’t have the data nor the experience to estimate the likelihood of default. They may also be missing some key pieces of the puzzle – for example, capital adequacy. But you may somewhat mitigate risks by choosing an entity that has any of the following (i) a more experienced regulator (ii) with a simpler business model (iii) being transparent, (iv) and systemically important.

In theory, brokers have capital requirements designed to cover administration costs if they collapse.

But it is possible that the capital held by the broker isn’t sufficient to cover the administration costs, for example if the broker also manages very illiquid securities that need to be valued by third party consultants. In this case, Investors may, depending on the insolvency regime, bear some administration costs. In the case of Beaufort Securities, this amount was in the hundreds of millions.

That is, unless the State decides to step in and cover the shortfall.

So, while more capital doesn’t always translate into the lower probability of default, brokers with larger market caps are under more scrutiny by regulators as they pose systemic risks, making bail-outs potentially more likely.