Why's Everyone Talking About It?

How Does It Impact Pre-Retirement Planning?

The Geeky Section 🤓

The 50% Local Equity / 50% International Equity Portfolio is compared against:

- ‘120-age in Equities Rule’ Portfolio: e.g. A 40-year-old French investor will hold 80% in French Equities and 20% in French Bonds. A variant is added by splitting the Equities equally into French/International.

- A Static 60/40: The French investor will have 60% in Equities, 40% in bonds. A variant is added by splitting the Equities equally into French/International.

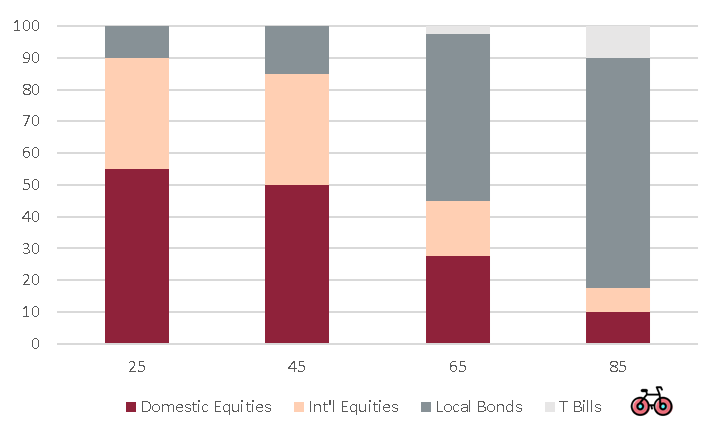

- A Target-Date Fund: With glide-path allocations, but most of it being in domestic securities, particularly at retirement where the International component is anecdotal. You can see the allocations below.

The Geeky Section 🤓

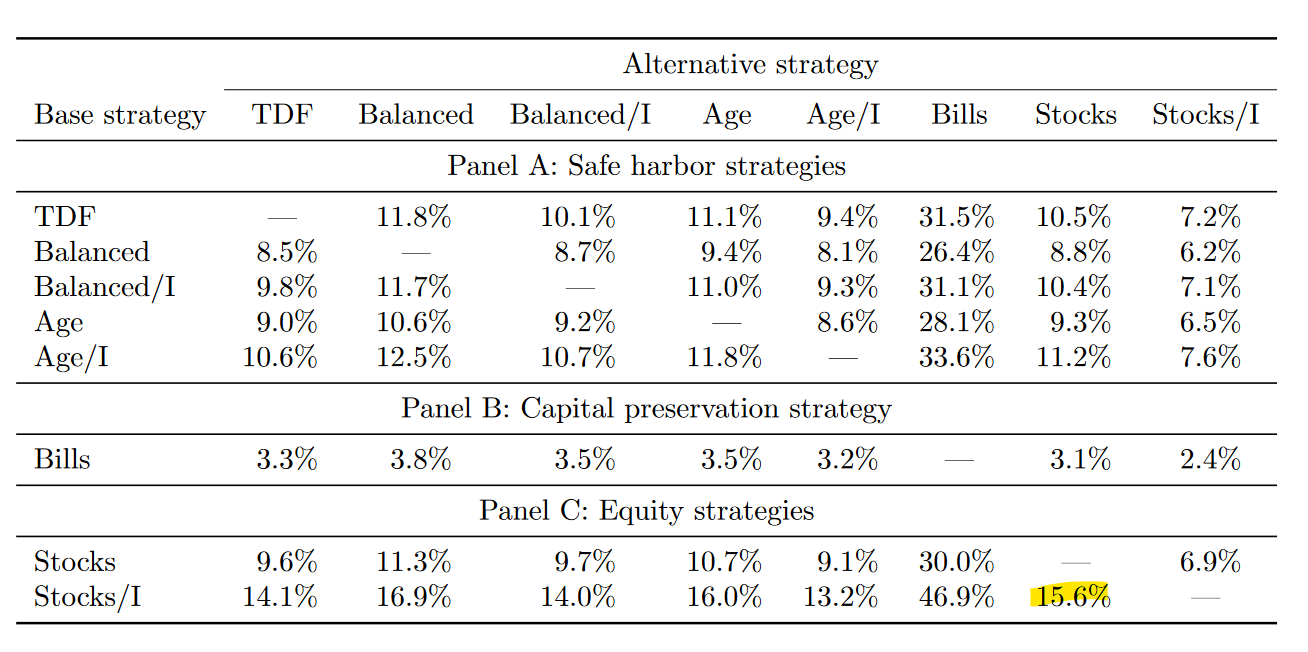

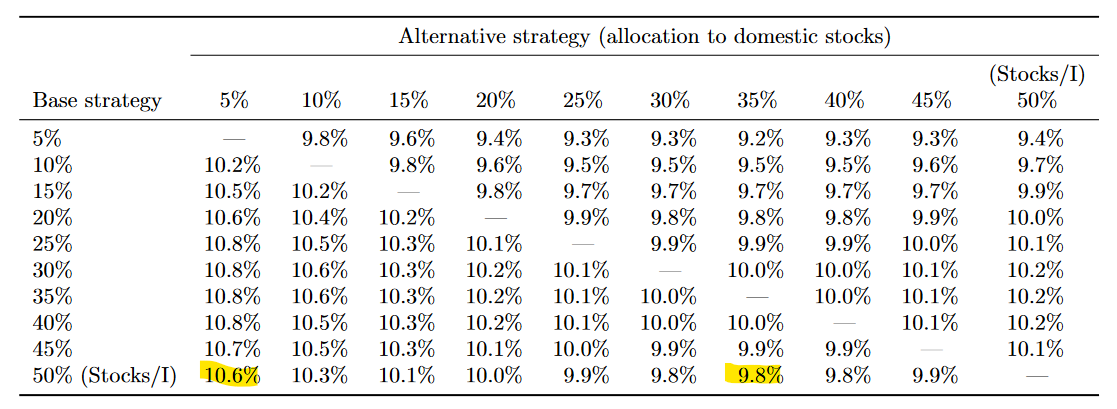

The below tables show the savings that an investor would need to deploy over his entire working life to produce the same impact, should he deviate from the Base Strategy (first column). The study baseline savings rate is 10%. What should you look at?

- ‘Stocks/I’ – is the 100% Stocks with 50% Domestic / 50% International Allocation

- ‘Stocks’ is the 100% Domestic Stock Allocation.

In the first table, the authors argue against a 100% Domestic Portfolio. If the Base Strategy is ‘Stocks/I’ (50/50 Portfolio) the investor would need to put aside a massive 56% more savings (15.6% vs. 10%) if he were to invest just in domestic stocks. The incentive to diversify globally is undeniable.

What about the case for some domestic bias? The appendix of the paper contains alternative asset allocations (not only 100% Domestic Stocks vs. 50% International/50% Domestic).

What we can read is that while the base case savings are still 10%, there is a 2% decrease in required savings if an investor reduced domestic stocks from 50% to 35% (9.8% vs 10%). So, a marginal decrease from 50% is even welcome. But, only a 6% increase (10.6% vs 10%) in required savings is needed to compensate for the decrease of domestic stocks allocation from 50% to 5%. In essence, statistical noise. Recall that the argument in favour of international diversification in the first table was ~10x stronger 56% more savings vs 6% more savings here. The paper does not prove any benefit of domestic stocks.

What about the theoretical perspective? The inflation narrative backing domestic bias is very weak. While it may have held true in the past (local firms served local markets), it lacks justification in today’s globalised and specialised economies. For example, pretty much the entire Danish Stock Market essentially serves obese people outside Denmark.

But, the case against home-bias comes also indirectly from the paper itself. 13 out of 38 countries in this sample had 80%+ declines, and some never recovered. Today, most European Markets are concentrated in a few firms/sectors and represent below 1% of global market capitalization. Greece has half of its market cap in just 4 banks that have been bailed out in the past. Would it be reasonable for the average investor to bet on Lithuanian or Portuguese Equities? At best, markets may sometimes not be liquid enough. At worst, it’s not hard to imagine a couple of local companies/industries derailing your retirement.

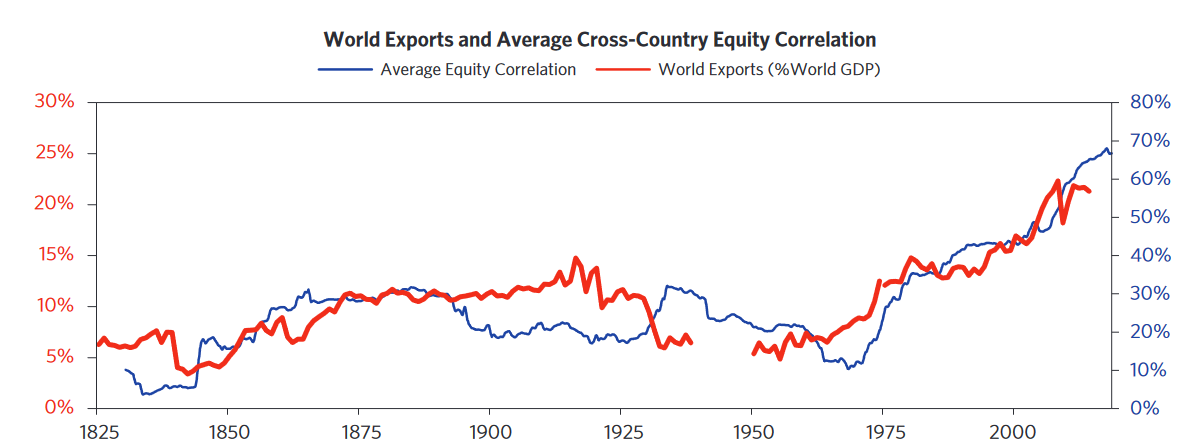

The Geeky Section 🤓

The chart below from Bridgewater shows equity correlations across countries against the size of exports as a percent of the global economy back to 1825. The surge of globalisation in the postwar era under US dominance, with rising trade and capital ties between countries globally, has led to unprecedented high correlations among the equity returns of different countries.

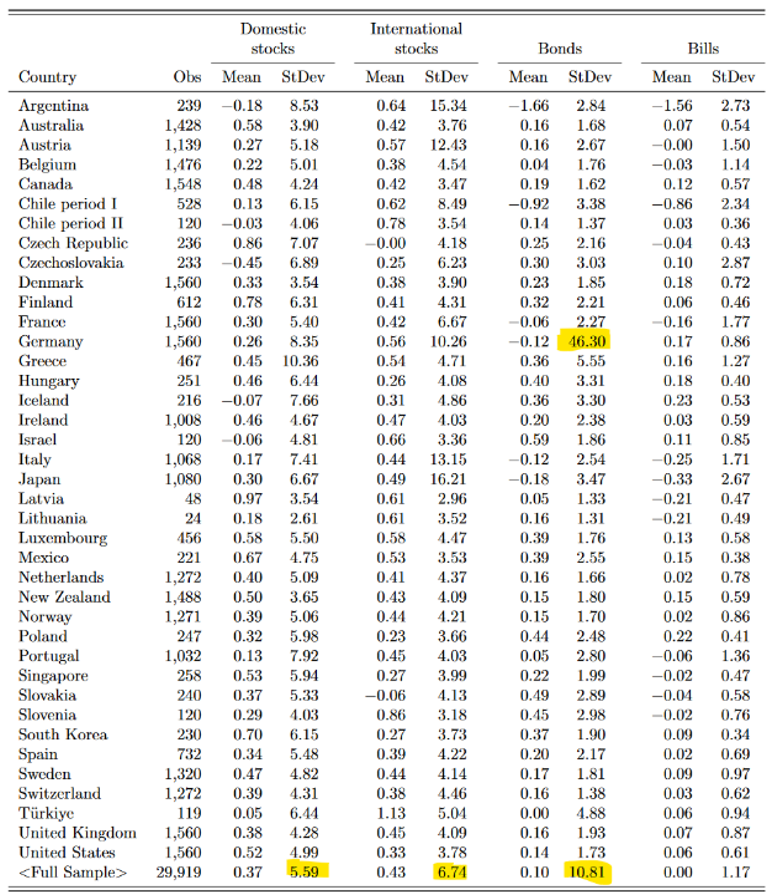

The Geeky Section 🤓

Germany Skewed Overall Numbers – While this paper omits the overall figures, the same dataset was published in the prior paper – which included the researchers’ data-cleaning project – including the overall figures. Overall volatility for all ‘Developed Market’ Bonds (10.81) is almost twice as high as for Equities (5.59). This is possibly skewed by absurd levels of hyperinflation in Germany (46.30) which other researchers exclude to make the research more appropriate for today’s investors.

The sample does a great job in stressing for inflationary periods. Average inflation seems to have been as persistent in the first and second half of the century (see averages below). But, even including COVID-19 spikes, today’s inflation data looks different – see my next point.

The Geeky Section 🤓

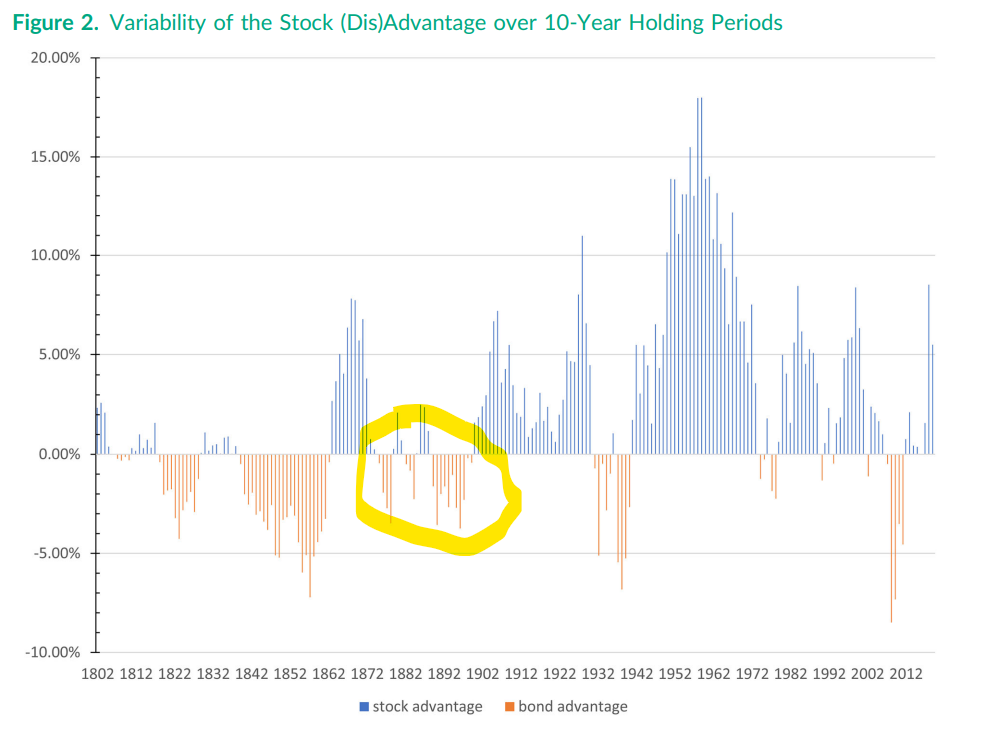

Evidence from other research – Despite the common belief in the superior long-term performance of stocks, Edward McQuarrie’s paper ‘Stocks for the Long Run? Sometimes Yes,

Sometimes No’ challenge this notion by presenting comprehensive data that goes back to the 19th century. His analysis reveals that outside the exceptional post-World War II period from 1941 to 1981, stocks in the U.S. have not consistently outperformed bonds. This pattern holds true even over extended investment periods, with a two-thirds chance of stocks outperforming bonds over 50 years, leaving a significant one-third chance for bonds to prevail. His analysis put an emphasis on regimes changes like the one highlighted below – a prolonged and global deflationary period caused by the industrial revolution.